Executive Summary

Rating: HOLD | EOSE

Measured from adjusted close on 2026-06-22 to 2026-08-06. Sell ratings are correct when the stock falls; Hold is tracked as a +/-10% range. Daily-close data, not intraday.

I would put my rating as a Hold because Eos Energy has a real manufacturing ramp, but the stock already discounts a cleaner path to self-funding scale than the cash flow profile supports. Revenue reached $57M in Q1 2026, yet TTM operating cash flow was -$302M and levered free cash flow was -$281.9M, so the equity still depends on outside capital while the business works toward positive operating margin.

Company Profile

Eos Energy Enterprises designs, manufactures and sells zinc-based battery energy storage systems for utility-scale, microgrid and commercial and industrial customers. It recognizes revenue when systems ship, or less often when they are delivered or commissioned. The company began commercializing in 2018, went public in 2020 through a SPAC merger, and operates one manufacturing facility in Turtle Creek, Pennsylvania, with Warrendale, Pennsylvania expected to come online in 2026. North America remains its core market.

Economic Moat

Business Model

I think Eos’s moat rests on the Z3 battery module, which is harder to replicate than a generic battery pack because it combines U.S. design, manufacturing, and a chemistry and mechanical architecture refined over more than 15 years. The module uses a simplified tub structure, about 50% fewer cells, and about 98% fewer welds than the prior Gen 23 product, so a competitor would need to copy both the product design and the manufacturing process at scale. The Battery Management System adds another layer of know-how because it monitors and balances the system in real time. Project American Made Zinc Energy, the DOE-backed manufacturing expansion, supports scale, but I view that as financing for the moat rather than the moat itself.

Business & Operating Risks

The biggest disclosed risk is still execution. Eos says it has limited experience in commercial manufacturing and has produced batteries only in limited quantities, which tells me the company has not yet proven that it can move from pilot output to repeatable volume. That matters because the business currently relies on a single Turtle Creek site, while Warrendale is not expected until 2026, so any disruption there would hit deliveries and revenue directly. Customer contract risk is also real: some arrangements may never become next-stage contracts, and many end customers depend on renewable-energy incentives that can change with policy.

Management Discussion & Analysis

Management is clearly prioritizing capacity over near-term earnings. Project American Made Zinc Energy is the capital-allocation center of gravity, and the DOE Loan Facility plus capitalized interest show that expansion is being funded with project-linked debt rather than only equity. I read the January 2025 full funding of the Delayed Draw Term Loan and the 2025 capital raises as a liquidity backstop, not as proof that the model is self-sustaining. The key question for me is whether that funding is buying time for a durable manufacturing ramp or simply extending the runway.

Recent Earnings

The latest quarter showed a sharp step-up in revenue and a much larger swing in EBITDA, which is encouraging but still not enough to call the operating model stable. Revenue eased to $57M in Q1 2026 from $58M in Q4 2025, so the business is scaling, but not yet in a smooth straight line. EBITDA moved from -$108M in Q4 2025 to $527M in Q1 2026, a swing that signals operating leverage, although I would want more disclosure before treating that as durable rather than quarter-specific. In my view, the moat is being tested by execution, not demand: the product appears differentiated, but the company still has to prove that it can manufacture it profitably at volume.

Financial Analysis

Growth

EOSE — Financial Growth (Quarterly, USD Mil)

| Metric | 2025-03-31 | 2025-06-30 | 2025-09-30 | 2025-12-31 | 2026-03-31 |

|---|---|---|---|---|---|

| REVENUE (USD Mil) | 10.5 | 15.2 | 30.5 | 58 | 57 |

| EBIT (USD Mil) | 21.9 | -218.1 | -636.3 | -113.8 | 521.1 |

| EBITDA (USD Mil) | 25 | -214.7 | -632.5 | -107.9 | 527.3 |

| NET INCOME (USD Mil) | 15.1 | -222.9 | -641.4 | -120.5 | 508.9 |

| DILUTED EPS | -0.2 | -1.1 | -4.9 | -0.8 | 0.1 |

Source: Yahoo Finance — Quarterly Financial Statements

Revenue rose from $10.5M in Q1 2025 to $57M in Q1 2026, a 442.9% year-over-year increase that shows the commercial ramp is real. The quarter-to-quarter path was uneven, though, moving from $15.2M in Q2 2025 to $30.5M in Q3 2025 and $58M in Q4 2025 before a slight pullback in Q1 2026. That pattern tells me the business is still lumpy, so investors should focus more on sustained run-rate improvement than on one quarter’s headline growth.

Profitability

EOSE — Profitability (TTM)

| Metric | TTM |

|---|---|

| Operating Margin (TTM) | -139.1% |

| Net Margin (TTM) | -296.1% |

| Return on Assets (TTM) | -33.5% |

| Return on Equity (TTM) | — |

Source: Yahoo Finance — Trailing Twelve Months (TTM)

TTM operating margin was -139%, net margin was -296%, and return on assets was -33.5%. Those numbers say Eos is still absorbing heavy fixed costs and financing costs before the business has reached scale. I weight operating margin most heavily because it shows whether the core battery operation is covering its own structure, and right now it is not. The important threshold is a positive operating margin, because that would show the company is finally covering its operating base rather than relying on external capital to bridge losses.

Valuation

EOSE — Valuation Multiples

| Metric | Value |

|---|---|

| Market Cap (USD Mil) | 2,597.3 |

| Enterprise Value (USD Mil) | 3,412.2 |

| Trailing P/E | — |

| Forward P/E | -161.3 |

| Price/Sales (TTM) | 16.2 |

| Price/Book (mrq) | -3 |

| EV/Revenue | 21.2 |

| EV/EBITDA | -12.8 |

| Beta (5Y Monthly) | 2.6 |

Source: Yahoo Finance

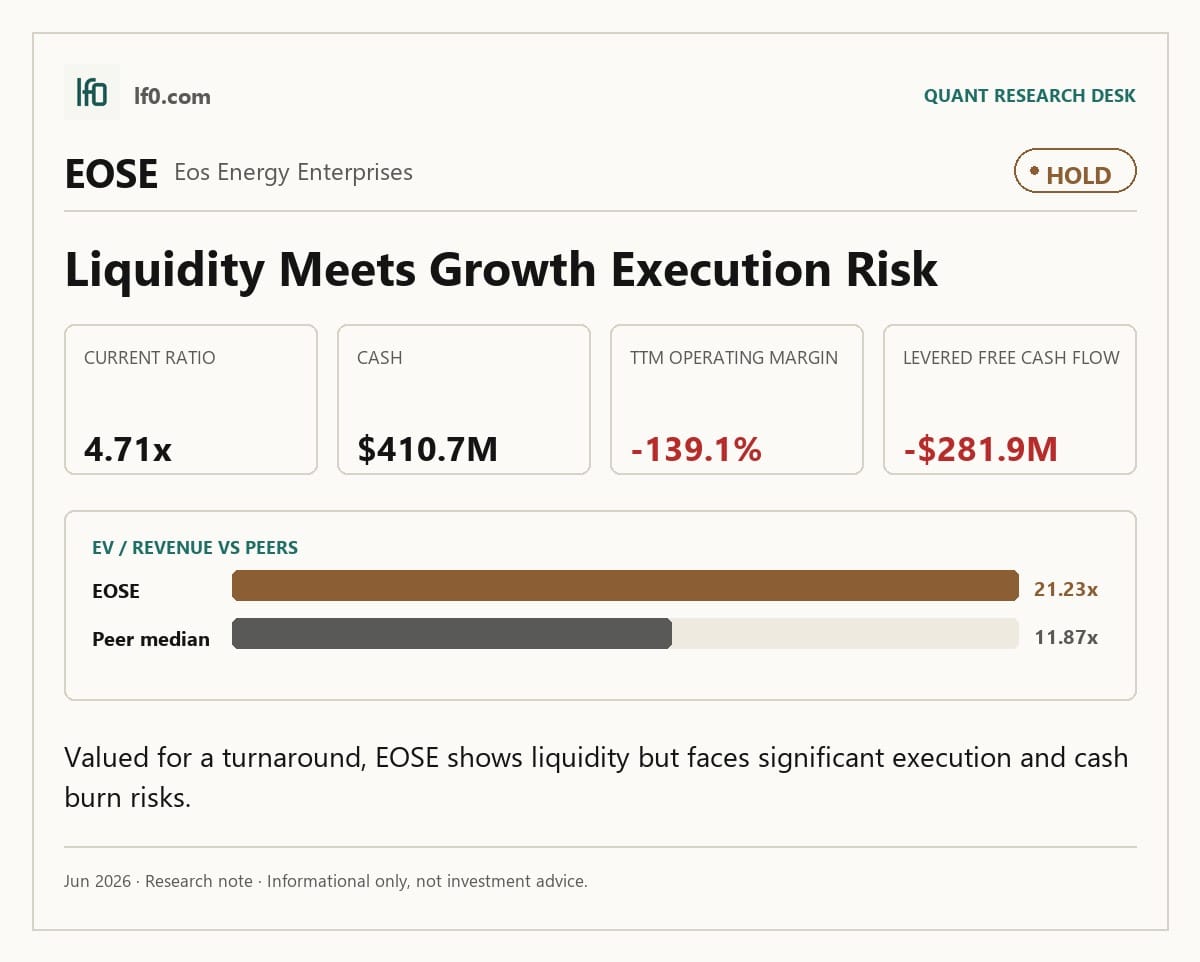

EOSE trades at 21.2x EV/revenue and 16.2x price/sales, with a forward P/E of -161x and EV/EBITDA of -12.8x, so earnings-based valuation is not yet useful. In my opinion, the market is paying for a turnaround that still needs proof in cash generation, not just for higher shipments. The stock also sits at -2.99x price/book, which reflects negative book equity from accumulated losses and makes book value a weak anchor. At a $2,597.3M market cap and 339.4M shares, the implied price is about $7.7, so the current valuation already assumes the ramp keeps improving while leverage stays manageable.

Leverage

EOSE — Leverage & Coverage (Quarterly)

| Metric | Value |

|---|---|

| Total Debt/Equity % (mrq) | — |

| Current Ratio (mrq) | 4.7 |

| Total Debt (mrq, USD Mil) | 642.9 |

| Operating Cash Flow (TTM, USD Mil) | -302 |

| Levered Free Cash Flow (TTM, USD Mil) | -281.9 |

Source: Yahoo Finance — Quarterly Financial Statements

EOSE has a 4.7 current ratio, $642.9M of total debt, -$302M of operating cash flow, and -$281.9M of levered free cash flow on a TTM basis. That is not a near-term liquidity crisis, but it is still a cash-burn story, so the cushion matters only if operating performance improves. The $410.7M cash balance helps, and the current ratio gives some breathing room, yet the debt load becomes more relevant if losses persist and the company has to refinance from a weaker position. I would view this as medium refinancing risk rather than distress, but the margin for error is thin.

Comparable Analysis

Growth

| Company | Revenue TTM (USD Mil) | Revenue Growth YoY % | EBITDA TTM (USD Mil) | Diluted EPS TTM |

|---|---|---|---|---|

| EOSE | 160.7 | 444.7% | -267.5 | -6.4 |

| FLNC | 2,584.6 | 7.7% | -18.4 | -0.3 |

| NXT | 3,559.4 | -4.7% | 738.2 | 3.8 |

| VRT | 10,843.4 | 30.1% | 2,383 | 4 |

| AMPX | 90.3 | 152.9% | -16.9 | -0.3 |

| BE | 2,449 | 130.4% | 231.6 | 0 |

Source: Yahoo Finance

EOSE’s TTM revenue growth of 444.7% is far above FLNC at 7.7%, NXT at -4.7%, VRT at 30.1%, AMPX at 152.9%, and BE at 130.4%. That pace is impressive, but it also comes off a much smaller base than the larger infrastructure names, which is why the market is still debating whether this is early scale or just early volatility. EOSE’s -267.5M EBITDA and -6.4 diluted EPS show that growth is not yet translating into earnings power.

Valuation

| Company | Trailing P/E | Forward P/E | EV/Revenue | EV/EBITDA | Price/Sales (TTM) | Price/Book (mrq) | Market Cap (USD Mil) | Enterprise Value (USD Mil) | Beta (5Y Monthly) |

|---|---|---|---|---|---|---|---|---|---|

| EOSE | — | -161.3 | 21.2 | -12.8 | 16.2 | -3 | 2,597.3 | 3,412.2 | 2.6 |

| FLNC | — | 123 | 1.3 | -184.2 | 1.8 | 8.9 | 4,570.9 | 3,398.5 | 2.8 |

| NXT | 32.8 | 21.6 | 5 | 24.1 | 5.4 | 8.1 | 19,159.9 | 17,826.2 | 1.7 |

| VRT | 83.3 | 37.6 | 11.9 | 54 | 11.8 | 32.3 | 127,927.4 | 128,691.8 | 2 |

| AMPX | — | 285.3 | 24.8 | -131.8 | 25.4 | 20.6 | 2,290.1 | 2,234.3 | 2.1 |

| BE | — | 75.7 | 38.4 | 406.1 | 38.2 | 101.5 | 93,556.4 | 94,044.4 | 3.7 |

Source: Yahoo Finance

EOSE trades at 21.2x EV/revenue and 16.2x price/sales, versus FLNC at 1.3x and 1.8x, NXT at 5.0x and 5.4x, VRT at 11.9x and 11.8x, AMPX at 24.8x and 25.4x, and BE at 38.4x and 38.2x. On that basis, EOSE is expensive relative to FLNC and NXT, but cheaper than AMPX and BE on headline revenue multiples. I think the comparison only makes sense when paired with leverage: EOSE’s 4.7 current ratio and $642.9M debt profile are less stretched than some peers, but the market is still paying for a business that has not yet shown positive operating margin. A $1 investment a year ago would be worth about $1.83 in EOSE today, well behind FLNC’s $4.41, AMPX’s $4.69, and BE’s $14.58 — EOSE’s 82.6% one-year return is real, but it already prices in a cleaner path to positive operating margin than the fundamentals above have delivered yet, which is the same gap this article’s rating is built on.

Profitability

| Company | Operating Margin (TTM) | Net Margin (TTM) | Return on Assets (TTM) | Return on Equity (TTM) |

|---|---|---|---|---|

| EOSE | -139.1% | -296.1% | -33.5% | — |

| FLNC | -8.4% | -1.6% | -1.3% | -12.7% |

| NXT | 18.2% | 16.5% | 12.2% | 29.6% |

| VRT | 16.4% | 14.4% | 11.1% | 45.1% |

| AMPX | -23.4% | -44.0% | -10.6% | -44.2% |

| BE | 9.6% | 0.2% | 3.1% | 1.3% |

Source: Yahoo Finance

EOSE’s operating margin of -139% and net margin of -296% are much weaker than FLNC at -8.4% and -1.6%, NXT at 18.2% and 16.5%, VRT at 16.4% and 14.4%, AMPX at -23.4% and -44.0%, and BE at 9.6% and 0.2%. Return on assets is also negative at -33.5%, which trails every profitable peer in the set. The gap tells me the issue is not just overhead; the unit economics still need to prove they can support scale.

Leverage

| Company | Total Debt/Equity % (mrq) | Current Ratio (mrq) | Total Debt (mrq, USD Mil) | Operating Cash Flow TTM (USD Mil) | Free Cash Flow TTM (USD Mil) |

|---|---|---|---|---|---|

| EOSE | — | 4.7 | 642.9 | -302 | -281.9 |

| FLNC | 8,773.1% | 1.4 | 402 | -236 | -133.7 |

| NXT | 226.6% | 2.4 | 52.9 | 562.9 | 311.7 |

| VRT | 7,691.3% | 1.5 | 3,264.9 | 2,577.3 | 1,964.8 |

| AMPX | 599.7% | 7.1 | 6.6 | -54.3 | -35.3 |

| BE | 31,147.6% | 5 | 2,952.8 | 298.2 | 265.5 |

Source: Yahoo Finance

EOSE’s 4.7 current ratio compares with FLNC at 1.4, NXT at 2.4, VRT at 1.5, AMPX at 7.1, and BE at 5.0. That liquidity cushion helps explain why the stock can carry a high valuation despite negative cash flow, but it does not erase the fact that operating cash flow is still -$302M TTM. In other words, the balance sheet buys time, while the operating model still has to earn the right to use that time.

Conclusion

I would put my rating as a Hold because Eos has enough liquidity to keep building, but not yet enough cash generation to justify a more aggressive call. The company’s 4.7 current ratio and $410.7M cash balance reduce near-term distress, yet TTM operating cash flow of -$302M and levered free cash flow of -$281.9M tell me the business still needs external funding while it scales. That is why I am not more bullish today: the market is already paying for a future in which manufacturing ramps cleanly and margins improve, but the current numbers do not prove that path yet.

I would raise my rating toward Buy if Eos can keep quarterly revenue above $50M for several quarters and turn operating cash flow positive, because that would show the factory ramp is converting into self-funding scale rather than just higher shipments. A positive operating margin would matter even more, since it would mean the core battery business is finally covering its fixed cost base. If that happens while the current ratio stays near 4.7, the equity case becomes much easier to underwrite.

I would move from Hold to Sell if quarterly revenue falls back below $30M, because that would suggest the recent step-up was not durable and that demand or execution is less stable than the market assumes. I would also turn more cautious if cash burn stays near the current run rate, since that would keep pressure on the cash balance and make the $642.9M debt load more restrictive as refinancing dates approach.

After weighing both paths, I still think the burden of proof sits with management. The stock can work if the Q1 2026 margin swing proves durable, but until cash generation turns positive, I view the shares as a speculative hold rather than a fresh buy.

What’s your take? I rated Eos Energy Enterprises (EOSE) HOLD above — but the goal here is to get this right, not just to publish an opinion. What would you add to this analysis, or which risk or catalyst do you think I’m under- or over-weighting? Tell me in the comments.

Data sourced from Yahoo Finance. Not investment advice.

Leave a Comment