| Company | Jul 25 | Aug 25 | Sep 25 | Oct 25 | Nov 25 | Dec 25 | Jan 26 | Feb 26 | Mar 26 | Apr 26 | May 26 | Jun 26 | Trailing 12-Mo |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| HUT | +14.14% | +25.91% | +30.23% | +45.53% | -11.17% | +2.09% | +21.53% | -4.66% | -11.87% | +61.54% | +64.73% | -7.52% | +520.67% |

| CIFR | +14.23% | +39.93% | +64.79% | +48.13% | +9.12% | -27.47% | +8.13% | -2.26% | -17.50% | +37.84% | +33.31% | +3.59% | +412.55% |

| WULF | +17.81% | +83.14% | +20.85% | +35.73% | +0.06% | -25.92% | +16.36% | +21.32% | -11.04% | +50.59% | +17.63% | -3.36% | +463.93% |

| IREN | +10.57% | +64.37% | +77.23% | +29.45% | -21.30% | -21.00% | +42.28% | -23.80% | -16.29% | +32.76% | +39.62% | -28.03% | +213.86% |

| APLD | +30.49% | +21.61% | +43.55% | +51.09% | -21.81% | -9.52% | +38.17% | -19.51% | -12.94% | +44.27% | +38.04% | -21.11% | +270.41% |

| CORZ | -20.68% | +5.98% | +25.02% | +20.07% | -21.59% | -13.80% | +23.56% | -5.67% | -11.84% | +33.69% | +34.25% | -4.69% | +49.91% |

Source: Yahoo Finance monthly adjusted close. Each column is a fully completed calendar month; the current in-progress month is excluded. Trailing 12-Mo compounds the 12 monthly returns.

Executive Summary

Rating: SELL | HUT

I would put my rating as a Sell because Hut 8 is still valued for future infrastructure cash flow while the latest twelve months show a negative free cash flow yield of -2.7%, an EBITDA margin of -146.7%, and a current ratio of 0.9. The power footprint is real, with 1,020 MW under management across 15 sites as of December 31, 2025, but the market is already paying 41.3x EV/revenue for that optionality, so execution matters more than the asset base. I would move more constructive only if River Bend and the broader AI build start producing positive EBITDA and a clear step-down in free cash flow burn.

Company Profile

Hut 8 Corp. is an energy infrastructure platform that earns revenue from three layers: Power, Digital Infrastructure, and Compute. Power covers powered land, interconnects, substations, switchyards, and related electrical systems; Digital Infrastructure monetizes data centers through hosting, leasing, and colocation; Compute generates revenue from Bitcoin mining rewards, cloud and storage services, and AI cloud contracts. The company was incorporated in Delaware on January 27, 2023 for the Business Combination and lists its common stock on Nasdaq under HUT.

As of December 31, 2025, Hut 8 managed 1,020 MW across 15 sites in the United States and Canada, with 1,560 MW under development and construction. Its footprint includes five ASIC compute data centers, five traditional cloud and colocation data centers, one non-operational ASIC site, and the River Bend campus in Louisiana, a 330 MW AI data center targeted for Q2 2027. The platform also includes American Bitcoin, launched in 2025 and listed on Nasdaq under ABTC, plus Hut 8 Canada and Highrise AI.

Economic Moat

Business Model

Power access is the part of Hut 8 that I think is hardest for a competitor to copy quickly. The company has already assembled 1,020 MW of energy capacity under management across 15 sites in the United States and Canada, and that footprint is tied to interconnects, substations, switchyards, and powered land that take years to secure. I see the deeper advantage in the way Hut 8 monetizes that power through a vertically integrated stack, since it can move from power origination into digital infrastructure and then into compute without handing the economics to a third party. That gives the company more than one path to cash flow from the same asset base, even though the model still depends on execution and capital.

The business has shifted materially over the last five years. In fiscal 2025, prior filings showed a narrower Bitcoin mining and HPC platform, while the 2026 10-K shows a broader three-layer structure with Power, Digital Infrastructure, and Compute. The River Bend campus in Louisiana, a 330 MW AI data center under construction, is now the flagship AI project, while American Bitcoin added a public Bitcoin accumulation platform and Highrise AI added an AI cloud business with 1,000 NVIDIA H100 GPUs and 96 NVIDIA H200 GPUs. That evolution makes the business more diversified, but I would not call it more commercial yet because the latest twelve months still show negative operating cash flow and deeply negative EBITDA.

Business & Operating Risks

The River Bend buildout and the broader data center expansion program are the clearest disclosed risks because they can destroy value before a single dollar of revenue arrives. According to the risk factors in their SEC 10-K, the company is already “underway, or being contemplated” on expansions in new and existing markets, including a “15-year, 245 MW IT build to suit data center lease at our River Bend campus,” and the filing warns of construction delays, unexpected budget changes or cost overruns, permitting or regulatory hurdles, and delays in site readiness. Those are not abstract issues for Hut 8 Corp. because the latest financial data already shows the business leaning on capital-intensive growth while still posting negative free cash flow, so any delay would push out cash generation and raise the odds of dilution or project-level financing.

Liquidity and capital access are the next major headwind. The 10-K says the company may need to raise additional funds through equity or debt financings, that such financing may be unavailable in a timely manner or on acceptable terms, and that equity issuance would cause significant dilution. That risk is already showing up in the numbers: the company’s growth plan requires substantial capital before the new campuses produce revenue, so the balance sheet is part of the operating model, not a backstop. If credit markets tighten or equity valuations fall, the cost of funding River Bend and other projects rises immediately, which means investors are underwriting execution and financing at the same time.

Bitcoin concentration and American Bitcoin volatility are a third material risk, and this one has already affected results because the company’s quarterly earnings now swing with Bitcoin fair value under ASU 2023-08. The filing says the company is highly concentrated in Bitcoin, that Bitcoin is highly volatile, and that the value of the American Bitcoin equity stake may decline significantly, with possible impairment charges. The current filing also adds a new layer of risk: the company now holds 100 million World Liberty Financial, Inc. tokens with an indefinite lock-up, which adds another illiquid, policy-sensitive asset to an already crypto-heavy balance sheet. These risks do not break the moat itself, but they do threaten the speed and cost at which Hut 8 can turn its power footprint into durable cash flow.

Management Discussion & Analysis

Management is signaling a capital-heavy pivot toward AI data centers, and I think it is actively responding to the financing and execution risks above by locking in long-dated project debt and contracted counterparties. The clearest proof is the 15-year triple-net lease with Fluidstack for 245 MW of IT capacity at River Bend, with a base contract value of approximately $7B and potential to increase to $17.7B through renewal options. Google’s financial backstop covers the lease payments and related pass-through obligations for the initial 15-year base term, which lowers near-term counterparty risk, but it also locks Hut 8 into a large build obligation rather than a quick cash return.

Management is also steering capital toward project-level financing, saying River Bend is expected to be funded through a combination of cash, Bitcoin on the balance sheet, and project-level financing of up to 85% loan-to-cost, with J.P. Morgan and Goldman Sachs anticipated as loan underwriters. The sale of the 310 MW Far North portfolio to TransAlta, closed on February 2, 2026, and the prior five-year capacity contracts with the Ontario Independent Electricity System Operator Medium-Term 2 auction show management is recycling mature power assets into contracted infrastructure. I do not see the capital allocation as conservative: the company had borrowed the full $200.0 million under the Coinbase facility by December 31, 2025, had not drawn on the $200.0 million Two Prime revolving credit facility, and had issued 4,020,630 shares under the 2025 at-the-market program for gross proceeds of $183.4M at a weighted average issuance price of $45.62 per share.

The numbers partly support management’s claim that the compute pivot is working, but they also show how dependent the story is on Bitcoin and capital markets. Compute revenue rose to $202.3M in the twelve months ended December 31, 2025 from $80.7M in the prior twelve months, driven by a higher average revenue per Bitcoin mined of $103,647 and 1,803 Bitcoin mined; that is real operating progress, not just narrative. At the same time, adjusted EBITDA was negative -$135.4M in the twelve months ended December 31, 2025, after being $555.7M in the prior period, so the growth in compute did not translate into durable earnings power once digital asset marks and expansion costs were included. The company’s KPI mix also shows a more selective posture, with energy capacity under diligence falling to 5,185 MW from 8,599 MW and capacity under exclusivity falling to 1,755 MW from 2,768 MW, while capacity under development rose to 1,230 MW from 0 MW.

Recent Events

The most significant development I see is the $3.25B senior secured notes deal priced on April 27, 2026 and closed on April 30, 2026, with 6.192% notes due 2042. Hut 8 is using the proceeds to fund the River Bend data center project in St. Francisville, Louisiana, including a 245 MW critical IT campus and substation, while also reimbursing prior equity contributions and building debt service reserves. In my view, that strengthens the thesis because it converts the company from a pure development story into one with a financed, lease-backed asset base and a long-dated liability structure.

The June 4, 2026 disclosure adds another layer: Beacon Point DC LLC priced a separate $4.25B offering of 6.129% senior secured notes due 2042 for a turnkey data center in Nueces County, Texas, with 352 MW of critical IT capacity. The tenant is described as a high-investment-grade counterparty rated AA- or higher, which is important because it ties the capital spend to a creditworthy lease rather than speculative capacity buildout. I read that as a meaningful validation of the platform, and it supports the view that Hut 8 is building contracted infrastructure rather than chasing open-ended crypto exposure.

The June 5, 2026 filing is mostly a pricing update on that Texas deal, so the signal is the same: repeated large-scale secured financing points to execution on a capital-intensive data center strategy. Recent events have materially strengthened the investment case by showing access to long-duration project debt and a clearer path to contracted cash flow.

Financial Analysis

Growth

HUT — Financial Growth (Quarterly, USD Mil)

| Metric | 2025-03-31 | 2025-06-30 | 2025-09-30 | 2025-12-31 | 2026-03-31 |

|---|---|---|---|---|---|

| REVENUE (USD Mil) | 21.8 | 41.3 | 83.5 | 88.5 | 71 |

| EBIT (USD Mil) | -147.1 | 173.5 | 78.2 | -374.4 | -292.8 |

| EBITDA (USD Mil) | -131.5 | 193.6 | 106.7 | -334 | -253.7 |

| NET INCOME (USD Mil) | -133.9 | 137.3 | 50.1 | -279.7 | -219.8 |

| DILUTED EPS | -1.3 | 1.2 | 0.4 | -2.5 | -2 |

Source: Yahoo Finance — Quarterly Financial Statements

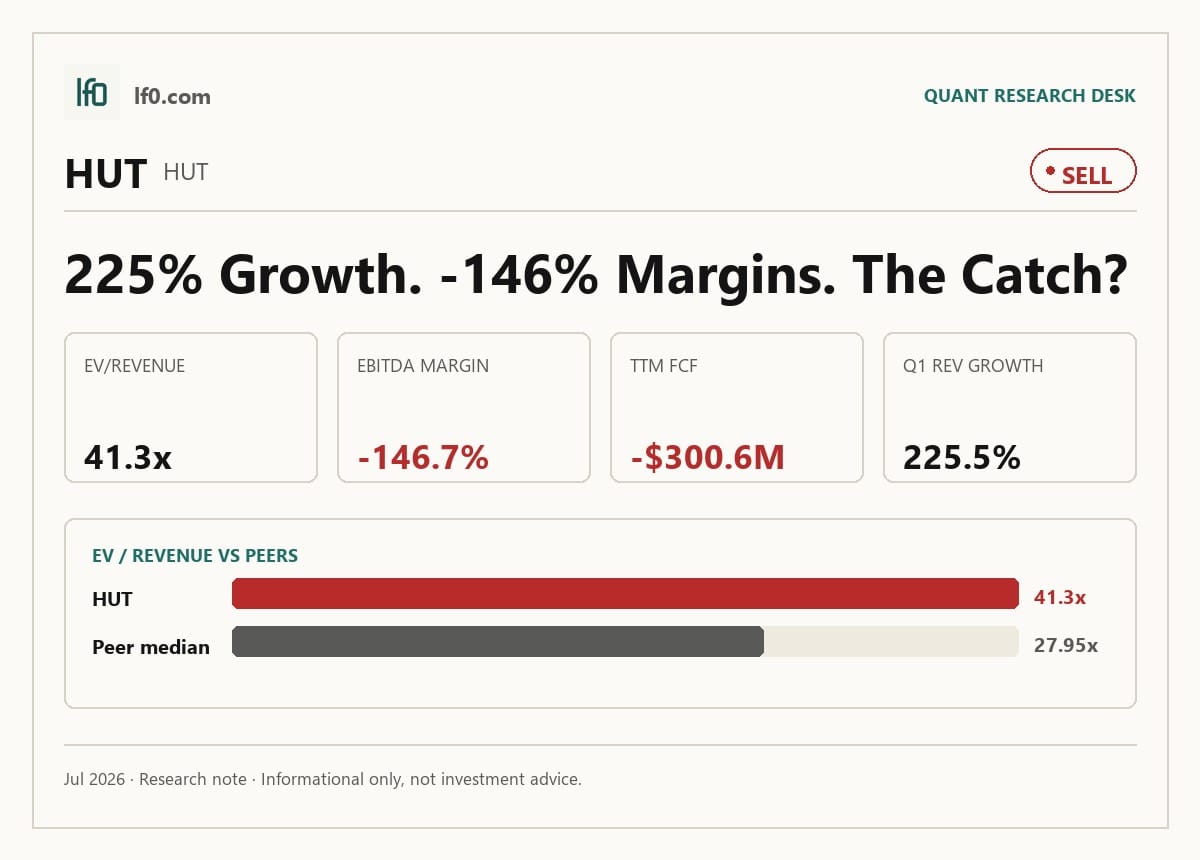

Hut 8’s revenue rose from $21.8M in Q1 2025 to $71M in Q1 2026, which is a 225.5% year-over-year increase, but the sequential path was uneven because revenue peaked at $88.5M in Q4 2025 before easing in the next quarter. EBITDA moved even more sharply, from -$132M in Q1 2025 to $194M in Q2 2025 and then back to -$254M in Q1 2026, so the business is still too volatile for me to call the growth durable. The growth profile supports the moat thesis only if the new power and data center assets can turn scale into steadier earnings, not just bigger top-line swings.

Profitability

HUT — Profitability (TTM)

| Metric | TTM |

|---|---|

| Operating Margin (TTM) | -521.5% |

| Net Margin (TTM) | -109.8% |

| Return on Assets (TTM) | -16.2% |

| Return on Equity (TTM) | -27.4% |

| Gross Margin (TTM) | 59.7% |

| EBITDA Margin (TTM) | -146.7% |

Source: Yahoo Finance — Trailing Twelve Months (TTM)

TTM gross margin of 59.7% shows Hut 8 is not losing money at the revenue line, but the TTM EBITDA margin of -146.7% and operating margin of -521.5% show overhead, development spend, and non-cash charges are overwhelming that gross profit. The gap between gross margin and EBITDA margin is so wide that I focus on whether River Bend and the broader AI infrastructure pipeline can absorb fixed costs, not on the current gross profit rate alone. TTM net margin of -109.8%, TTM ROA of -16.2%, and TTM ROE of -27.4% all point to an early-stage platform still burning capital rather than compounding it.

Valuation

HUT — Valuation Multiples

| Metric | Value |

|---|---|

| Market Cap (USD Mil) | 11,134 |

| Enterprise Value (USD Mil) | 11,739 |

| Forward P/E | -53.2 |

| Price/Sales (TTM) | 39.2 |

| Price/Book (mrq) | 8.1 |

| EV/Revenue | 41.3 |

| EV/EBITDA | -28.1 |

| Beta (5Y Monthly) | 6.07 |

| FCF Yield % (TTM) | -2.7% |

| Forward EPS (USD) | -1.9 |

| Analyst Target Price – Low (USD) | 70 |

| Analyst Target Price – Mean (USD) | 129.9 |

| Analyst Target Price – High (USD) | 226 |

| # Analyst Opinions | 16 |

Source: Yahoo Finance

Hut 8 screens on revenue and cash flow, not earnings, because the latest twelve months show a negative trailing P/E, a negative forward P/E of -53.2x, and an EV/EBITDA of -28.1x. The primary anchor is EV/revenue at 41.3x, which implies the market is paying for a very large step-up in monetization from the current $2.648 of revenue per share to something closer to infrastructure-like recurring cash flow as River Bend and the AI data center pipeline come online. Price/sales of 39.2x points to the same conclusion, and the 8.07x price/book ratio is rich for a business with a book value per share of $12.26, so investors are paying well above accounting equity for future capacity rather than current assets.

I would put fair value in a wide range of roughly $48-$193 per share based on peer EV/revenue multiples and the leverage profile here, but that range is not a clean consensus because the 16 analyst opinions span a much broader $70-$$226 target range with a $129.9 mean. My range sits below the analyst mean because I weight the negative free cash flow yield and the still-negative EBITDA margin more heavily than the market seems to. On earnings, I would frame the stock around a forward EPS range that remains negative until the buildout starts to convert, and that is why the current -$1.86 forward EPS matters: it tells me the equity is still priced ahead of earnings rather than alongside them. Relative to peers, that makes HUT look expensive on a like-for-like basis because the market is paying for future EPS improvement before the company has shown it can sustain positive operating leverage.

FCF yield is -2.7%, with levered free cash flow of -$300.6M in TTM, or about -$2.7 per share, which means the stock is being valued despite ongoing cash burn. Beta is 6.07, so the multiple also embeds very high execution risk. Analyst coverage is 16 opinions, with targets from $70 to $226 and a $129.9 mean. I think the valuation still reflects optionality more than proof.

Leverage

HUT — Leverage & Coverage (Quarterly)

| Metric | Value |

|---|---|

| Total Debt/Equity % (mrq) | 25 |

| Current Ratio (mrq) | 0.9 |

| Total Debt (mrq, USD Mil) | 422.9 |

| Operating Cash Flow (TTM, USD Mil) | -132.6 |

| Levered Free Cash Flow (TTM, USD Mil) | -300.6 |

| Net Debt/EBITDA (TTM) | -0.6 |

| FCF Margin % (TTM) | -105.7% |

Source: Yahoo Finance — Quarterly Financial Statements

Hut 8 carries $422.9M of total debt against a current ratio of 0.9, so near-term liquidity is not abundant. Operating cash flow was -$132.6M TTM and levered free cash flow was -$300.6M TTM, which means EBITDA is not converting into cash yet and the business is still absorbing capital rather than funding itself. Net debt/EBITDA was -0.6x TTM, helped by cash on hand, and FCF margin was -105.7% TTM, a clear sign that cash burn is running well ahead of revenue generation.

Total debt/equity was 25.02% mrq, which is not a balance-sheet stress point by itself, but the negative cash flow profile means that cushion can erode if project spending stays elevated. In my opinion, this is medium refinancing risk because the current ratio gives some short-term room, yet persistent negative operating cash flow would make the next funding step more important if capital needs stay high. Leverage is manageable today, but cash burn leaves limited financial flexibility.

Insider Activity

The insider transaction record I see here is one-sided: 7 open-market sales, $7.1M total value, and no open-market purchases in the 2025-03-28 to 2026-05-21 window. The selling is also broad, not just one insider, because a director, the chief legal officer, and the chief financial officer all sold, which suggests weak alignment between insiders and shareholders at the current price. I would not overread insider ownership on its own, but the trading pattern is still a bearish signal.

Comparable Analysis

Growth

| Company | Revenue TTM (USD Mil) | Revenue Growth YoY % | EBITDA TTM (USD Mil) | Diluted EPS TTM |

|---|---|---|---|---|

| HUT | 284.3 | 225.5% | -417.1 | -2.7 |

| CIFR | 209.8 | -28.8% | 165.8 | -2.1 |

| WULF | 168.1 | -1.1% | -143.9 | -2.5 |

| IREN | 757.1 | -0.0% | 147.2 | 0.7 |

| APLD | 319.3 | 139.3% | 13.9 | -0.4 |

| CORZ | 354.7 | 44.9% | -96.7 | -3.4 |

Source: Yahoo Finance

HUT’s revenue growth of 225.5% in the latest quarter stands out against the peer set, with APLD at 139.3%, CORZ at 44.9%, IREN at -0.0%, WULF at -1.1%, and CIFR at -28.8%. The catch is that HUT’s growth is coming off a smaller base and still pairs with negative EBITDA, so the market is paying for scale-up that is not yet stable. That is why I view the growth lead as real but not yet monetized.

Valuation

| Company | Trailing P/E | Forward P/E | EV/Revenue | EV/EBITDA | Price/Sales (TTM) | Price/Book (mrq) | Market Cap (USD Mil) | Enterprise Value (USD Mil) | Beta (5Y Monthly) | FCF Yield % (TTM) | Forward EPS | Analyst Target Price – Low | Analyst Target Price – Mean | Analyst Target Price – High | # Analyst Opinions |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| HUT | — | -53.2 | 41.3 | -28.1 | 39.2 | 8.1 | 11,134 | 11,739 | 6.07 | -2.7% | -1.9 | 70 | 129.9 | 226 | 16 |

| CIFR | — | 41.9 | 58.5 | 74 | 39.2 | 11.4 | 8,230 | 12,273 | 3.20 | -35.8% | 0.5 | 23 | 32.6 | 69 | 16 |

| WULF | — | 100.9 | 77.6 | -90.6 | 58 | -106.4 | 9,752 | 13,037 | 4.26 | -2.9% | 0.2 | 30 | 38.6 | 72 | 17 |

| IREN | 52.5 | -40.8 | 20.7 | 106.6 | 18.1 | 4.9 | 13,698 | 15,682 | 4.28 | -16.9% | -0.9 | 41 | 80.9 | 126 | 15 |

| APLD | — | -22.9 | 32.3 | 742.5 | 25.3 | 5.1 | 8,063 | 10,325 | 5.68 | -18.6% | -1.2 | 48 | 76.7 | 106 | 10 |

| CORZ | — | 75.1 | 23.6 | -86.5 | 20 | -5.4 | 7,079 | 8,370 | 5.50 | 2.5% | 0.3 | 27 | 33.4 | 55 | 16 |

Source: Yahoo Finance

HUT trades at 41.3x EV/revenue and 39.2x price/sales, versus CORZ at 23.6x and 20.0x, APLD at 32.3x and 25.3x, IREN at 20.7x and 18.1x, and CIFR at 58.5x and 39.2x. HUT’s FCF yield of -2.7% is better than CIFR’s -35.8% and APLD’s -18.6%, but it is still negative, so the stock is not being supported by cash generation. On a growth-adjusted basis, I think the market is already paying HUT for a cleaner earnings path than the company has actually delivered.

Profitability

| Company | Operating Margin (TTM) | Net Margin (TTM) | Return on Assets (TTM) | Return on Equity (TTM) | Gross Margin (TTM) | EBITDA Margin (TTM) |

|---|---|---|---|---|---|---|

| HUT | -521.5% | -109.8% | -16.2% | -27.4% | 59.7% | -146.7% |

| CIFR | -249.4% | 0.0% | -0.2% | -121.7% | 12.4% | 79.0% |

| WULF | -366.2% | 0.0% | -3.4% | -2,215.9% | 64.0% | -85.6% |

| IREN | -64.5% | 20.9% | -3.0% | 7.7% | 68.4% | 19.4% |

| APLD | -20.5% | -59.5% | -0.6% | -5.6% | 45.4% | 4.4% |

| CORZ | -18.8% | 0.0% | -4.3% | — | 21.6% | -27.3% |

Source: Yahoo Finance

HUT’s gross margin is 59.7%, above APLD’s 45.4% and well above CIFR’s 12.4%, but its EBITDA margin is -146.7%, worse than CORZ at -27.3% and APLD at 4.4%, and its operating margin of -521.5% is the weakest in the group. That combination points to a scale and opex problem, not a cost-of-revenue problem, because HUT is keeping more than half of revenue after direct costs but still cannot absorb overhead. I read that as a sign that the business model has not yet reached operating leverage.

Leverage

| Company | Total Debt/Equity % (mrq) | Current Ratio (mrq) | Total Debt (mrq, USD Mil) | Operating Cash Flow TTM (USD Mil) | Free Cash Flow TTM (USD Mil) | Net Debt/EBITDA (TTM) | FCF Margin % (TTM) |

|---|---|---|---|---|---|---|---|

| HUT | 25 | 0.9 | 422.9 | -132.6 | -300.6 | -0.6 | -105.7% |

| CIFR | 641.6 | 3.1 | 4,746.7 | -69.2 | -2,948.1 | 24.3 | -1,405.0% |

| WULF | — | 1.2 | 5,314.1 | -197.3 | -283.3 | -18.7 | -168.6% |

| IREN | 148.8 | 3.7 | 3,964.9 | 392.5 | -2,311 | 11.9 | -305.3% |

| APLD | 110.1 | 2.4 | 2,827.5 | -36 | -1,496.9 | 78.9 | -468.9% |

| CORZ | — | 0.5 | 2,155.5 | 573.2 | 175 | -11.9 | 49.3% |

Source: Yahoo Finance

HUT’s debt/equity is 25.02%, far below CIFR’s 641.6% and APLD’s 110.1%, but its current ratio is only 0.9 and free cash flow margin is -105.7%, so liquidity is tighter than the raw debt ratio suggests. Net debt/EBITDA of -0.6x is mathematically helped by negative EBITDA, which makes it less informative than the cash burn figure; the more useful read is that HUT burned -$300.6M of free cash flow TTM, or about -$2.7 per share. That is why the lower leverage does not translate into a lower-risk equity in practice.

Conclusion

I would put my rating as a Sell because the bull case still depends on several things going right at once: project delivery, financing, and a cleaner conversion from revenue to cash. The stock can keep working if those pieces line up, but until I see positive EBITDA and a real reduction in cash burn, I think the market is ahead of the business rather than the other way around.

I would raise my rating more towards a Buy if River Bend and the broader AI build start producing positive EBITDA and free cash flow, because that would show the platform is finally absorbing its fixed cost base. A useful threshold is a positive EBITDA margin and a clear step-down in levered free cash flow burn from the current -$300.6M TTM, since even a $150M improvement would cut the cash drain roughly in half and materially improve the financing outlook. If revenue also holds above the Q1 2026 level of $71M for several quarters while the 200-day moving average of $65.62 is reclaimed and sustained, I would read that as confirmation that the market is not just chasing a short squeeze.

I would move from Sell to Strong Sell if the company keeps funding growth with dilution while operating cash flow stays negative and the River Bend timeline slips, because then the equity would be paying for delay rather than for capacity. The most damaging version of that bear case is simple arithmetic: if levered free cash flow remains near the current -$300.6M TTM and the next large project slips by a year, Hut 8 gives up a year of contracted revenue while still carrying the build cost, which pushes the financing burden onto shareholders before the asset base earns its keep. A second warning sign would be another round of insider selling on top of the 7 open-market sales already disclosed, because that would reinforce the view that management is monetizing the stock while investors are underwriting the risk.

Weighing both sides, I lean bearish because the bull case still depends on project delivery, financing, and a cleaner conversion from revenue to cash. The stock can keep working if those pieces line up, but until I see positive EBITDA and a real reduction in cash burn, I think the market is ahead of the business rather than the other way around.

What’s your take? I rated Hut 8 (HUT) SELL above — but the goal here is to get this right, not just to publish an opinion. What would you add to this analysis, or which risk or catalyst do you think I’m under- or over-weighting? Tell me in the comments.

Sources

- SEC 10-K Annual Report — filed 2026-02-25

- SEC 8-K Filing (2026-06-05)

- SEC 8-K Filing (2026-06-04)

- SEC 8-K Filing (2026-05-06)

- SEC 8-K Filing (2026-05-01)

- SEC 8-K Filing (2026-04-28)

- SEC 8-K Filing (2026-04-27)

- SEC Form 4 Insider Transaction (2026-05-26)

- SEC Form 4 Insider Transaction (2026-05-13)

- SEC Form 4 Insider Transaction (2026-05-04)

- SEC 10-K Annual Report — FY2026

- SEC 10-K Annual Report — FY2025

Data sourced from Yahoo Finance and SEC EDGAR. Not investment advice.

Leave a Reply